A big part of running a restaurant is constantly making decisions. Do you want to serve chicken burgers or a plant-based menu? Do you rent a location in the heart of downtown or a little outside? Casual or formal uniforms?

Then there are decisions about payments – you need to provide payment options for your guests. So which payment processor do you go with? And which pricing model do they use – fixed rates or cost plus pricing? Which is right for your restaurant? And what do all of these terms even mean?

It’s definitely a decision that’s a bit more technical than menu choices or uniforms but just as important for a well-rounded business plan. The key to making the right decision is knowing the difference between the two most popular pricing models, as well as the pros and cons of both, so you can make an informed decision.

So, what do you need to know about these pricing models to ensure you’re making the right choice for your restaurant? We’ll go over:

- What a payments pricing model is

- The basics of payment processing fees and pricing models

- The breakdown of fixed rates and cost plus payment processing plans

- The pros and cons of both

Let’s get started!

What We Mean by “Payment Pricing Model”

When we talk about payment pricing models, we’re referencing how individual payment processors structure their payment processing fees (i.e. what you get charged for each transaction). This can range from completely flat fees that always stay the same to fluctuating fees, based on a number of factors (which we’ll get into later).

For a full explanation of all the ins and outs of payment processing fees, you can check out The Ultimate Guide to Payment Processing for Restaurants. You’ll learn all about the types of fees they charge, including flat, situational, and processing.

There’s not a lot a restaurant owners can do about flat and situational fees, but when it comes to processing fees – the bulk of what you pay a payment processor – you have a few choices to make about how you pay them.

Payment Processing Fees: The Basics

Before we get into pricing model choices, it’s important to understand a key component of processing fees: the interchange rate.

Every credit card brand (e.g. Mastercard, Visa) has a published, percentage-based interchange fee that they charge a merchant every time one of their cardholders uses their credit card. It’s the cost of authorizing the charge. For example, the interchange for a debit card, around 0.03%, is much less than a credit card, about 1.81%.

No merchant or payment processor is able to modify a credit card’s interchange rate, but there are three variables that are part of the decision when payment processors set processing rates:

- The type of credit card

- The type of payment

- The size of your business

These three factors come into play when it’s time to choose a pricing model, so it’s important to understand them and how they impact these rates!

Insider Tip: While some payment processors will offer significant discounts to merchants with larger businesses (i.e. chains, grocery stores, etc.), TouchBistro offers merchants of all sizes the same transparent rates with our cost plus pricing model. That means independent restaurants get access to the best payments service and the best rates.

1) Type of Credit Card

When it comes to credit cards, there are a lot of choices for consumers. Student cards, no-fee cards, low-fee cards, rewards cards, platinum cards, travel cards… you name it and there’s a credit card out there for it.

But did you know that each type of card comes with a different rate for processing it? This is a fee that the merchant pays every time you use that card.

Put simply, the more features a card has, the higher it costs a merchant to process the transaction. For example, a platinum travel card with features for the cardholder like travel insurance and high rewards points will have a higher interchange fee than a basic student credit card, which has no features or benefits.

2) Type of Payment

Similar to the type of card, the way you pay is also a factor when processors consider fees. Swiping, dip and signing, tapping, mobile payments, and other methods of payment are not created equal.

Basically, the more secure the form of payment, the cheaper the processing fee per transaction. For example, swiping costs more than mobile payments because there’s a higher risk of fraud. EMV chip cards cost less than traditional debit and credit cards because there’s an extra layer of security built right in.

The most expensive type of transaction is a “card not present,” like when a credit card payment is processed over the phone. This carries the highest risk of fraud.

3) Type of Retailer

It may not seem fair, but the bigger your operation, the better the discount you’ll get from payment processors. That’s because they offer a discount for a high volume of transactions.

Thriving retailers like franchised supermarkets will have some of the lowest processing fees because they have a guaranteed high number of transactions. In contrast, the local coffee shop that’s only open on weekdays will likely pay higher rates because they have significantly fewer transactions. This is why some smaller merchants try to get back higher costs by charging a transaction fee for using a credit card on purchases under a certain dollar amount.

Pricing Models: The Options

Now that we understand some of the factors that go into the processing fees, let’s uncover the pricing models that are available to restaurant owners.

The two most popular are fixed rates and cost plus (also known as interchange plus) pricing models. Let’s walk through both of them.

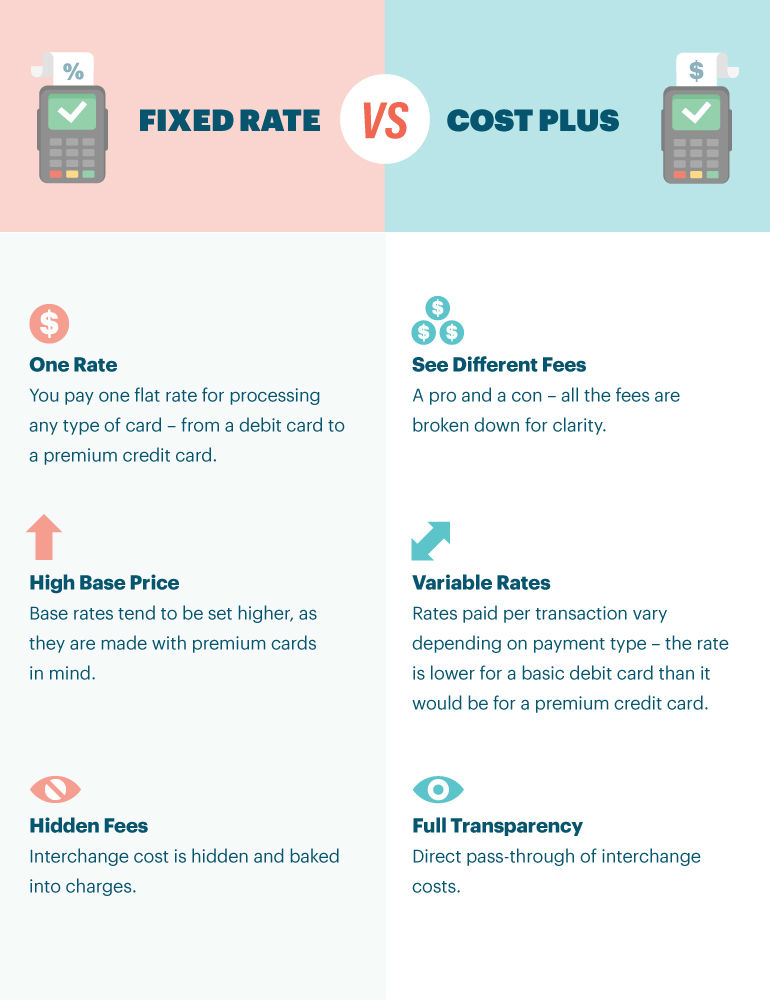

Fixed Rate Pricing Model

Sometimes restaurant owners choose this pricing model because it seems like the most straightforward option.

And it is.

With this pricing model, the payment processor charges a percentage-based fee plus a fee per transaction. It doesn’t matter what type of card is used (i.e. a student card vs. a platinum card) or the method of payment (i.e. swipe vs. digital payment). Here’s an example:

Flat Fee Rate (2.49%) + Transaction Fee ($0.15) = total processing fees

And here’s what that looks like on a $100 restaurant check:

($100 x 2.49%) + $0.15 = $2.64 total processing fees

The fixed rate model is simple and predictable, which is appealing to restaurant entrepreneurs and independent restaurant owners because they want to know what to expect when it comes to operating costs.

However, there are more than a few downsides to the fixed rate model.

1) Payment Processors Set High Rates

Remember the fluctuating interchange fees associated with the type of card and type of payments? Payment processors don’t want to pay any more than they have to, so they tend to set higher fixed rate processing fees to cover that.

The cost of processing a basic, no-fee card using a secure method of payment costs them the same as processing a platinum card over the phone. But merchants pay the same rate no matter what. There’s profit to be had in those margins, but it doesn’t go to the restaurant owner.

2) Rates Can Be Raised at Any Time

When they set their fixed rate, payment processors base it on a forecast of the customer demographics of each merchant and and the type of cards or methods of payment they expect the merchant to accept. If they find that their predictions were off and they believe they’re losing money, they can jack up the fixed rate whenever they choose.

If the rate isn’t as favorable to the processor as it is to the merchant, they will usually raise the cost. And there’s nothing the restaurant owner can do about this – the right to raise the rate without warning or negotiation is built into most contracts.

3) No Discounts for Lower Cost Cards

Under the fixed rate model, you’re not able to take advantage of the interchange fees associated with basic cards like no-fee credit cards and debit cards. If your customer base typically pays with these types of cards (for example, you serve a lot of students), it’s almost guaranteed that you’re paying more per transaction than you could be.

When you consider the bigger picture of the fixed rate model, it becomes clear that it’s worth investigating other options to find a better deal.

Cost Plus Pricing Model

Cost plus (or interchange plus) pricing is considered the most popular and most transparent pricing model available for merchants. With easy-to-understand terms and fees, many merchants see it as a more equitable option. These very benefits are the reason TouchBistro leads the marketplace with cost plus pricing.

With the cost plus pricing model, the restaurant owner pays the non-negotiable interchange fee (for the type of credit card, like Mastercard or Visa) and the payment processor markup. The markup is calculated by adding the interchange fee, basis point mark-up, and a per-transaction fee charged by the payment processor.

Here’s what that looks like:

Interchange fee + basis point mark-up + transaction fee = total processing fee

And here’s what that looks like for a $100 restaurant check:

Interchange fee (1.8%) + Basis point mark-up (0.45%) + Transaction Fee ($0.15) = total processing fees

($100 x 2.25%) + $0.15 = $2.40 total processing fees

Compare this equation to the fixed rate pricing model above, and you can see where it’s possible to save money on every transaction.

Fixed Rate Pricing Model

($100 x 2.49%) + $0.15 = $2.64 total processing fees

vs

Cost-Plus Pricing Model

($100 x 2.25%) + $0.15 = $2.40 total processing fees

While $0.24 may not seem like much, imagine that loss multiplied by the number of transactions you go through every day. You could be losing out on hundreds of dollars per month.

Restaurant owners who serve customers who use a wide variety of card brands and card types are paying the lowest interchange rate possible on every transaction.

- Transparent: It’s transparent because the interchange rate for each card brand can be found on the card’s website – no surprises or changes.

- Equitable: It’s equitable because merchants are paying a custom rate for every transaction instead of a flat rate for all – no matter the type of card or method of payment.

With both fixed and cost plus pricing, payment processors require a merchant underwriting process to get a proper merchant account. Try to find a solution, like TouchBistro Payments powered by Chase, that provides the most straightforward application and approval process, so you can start accepting payments faster.

Though there are pros and cons to both pricing models, it’s important to note that you can change your mind. As long as you’re not locked into a contract and the partner supports both models, you can switch from fixed rate to cost plus (and vise versa).

No matter what route you choose, remember to work with payment processors that are backed by trusted financial institutions and offer a host of other benefits for your restaurant, including reporting and analytics, menu planning, next-day payments to your account, and much more.

Dana is the former Content Marketing Manager at TouchBistro, sharing tips for and stories of restaurateurs turning their passion into success. She loves homemade hot sauce, deep fried pickles and finding excuses to consume real maple syrup.

Learn how to save money on payment processing fees

Subscribe to the TouchBistro Newsletter

Your Complete Guide to Restaurant Reservations

Download Guide